Why the Gaming Industry is Spending Billions on Consolidation

Mohammed Omer Sharieff

Team Lead - Game Taxonomy

@Gameopedia

Read Time :

15 mins

The pandemic was a difficult time for the world, but a period of growth for gaming. The industry rose to prominence during COVID lockdowns – when millions turned to video games – and its biggest players are now consolidating at a rapid pace through high-profile mergers and acquisitions.

In this article we will discuss some of the transformative gaming deals of the past to provide context for the current spate in M&A, and delve into the motivations behind today’s high-profile acquisitions – companies are looking to penetrate lucrative gaming platforms, racing to create the metaverse, enriching gaming with cutting-edge technology, and incorporating vast user bases built around successful franchises. In addition, big tech companies like Meta, Netflix, and Amazon have become influential new entrants in the gaming space, seeking to expand their reach into metaverse development and Web3 marketplaces. In recent years, rising development costs and shifts in consumer spending have accelerated industry consolidation. A decade ago, the industry’s approach to consolidation and M&A was less aggressive, but the landscape has evolved significantly. We will conclude with a discussion of how the industry appears to be entering a period of mega-consolidation, driven by rising development costs, the need for larger audiences to make games profitable, and changes in consumer spending habits post-pandemic.

How Explosive Growth in Gaming is Powering Consolidation

The industry registered record growth during COVID – people restricted to their homes sought to entertain themselves and stay connected, and gaming enabled them to do both – as more users played multiplayer games, time spent on gaming and related activities increased by 39%. No surprise, then, that the gaming market was valued at $198.40 bn in 2021, and is expected to be worth nearly $340 bn by 2027, with mobile games revenue expected to cross $100 bn by 2023. The gaming industry is larger than the movie and music industries combined.

While the COVID-19 pandemic initially boosted the gaming industry, the return to pre-pandemic trends has led to a slowdown and layoffs.

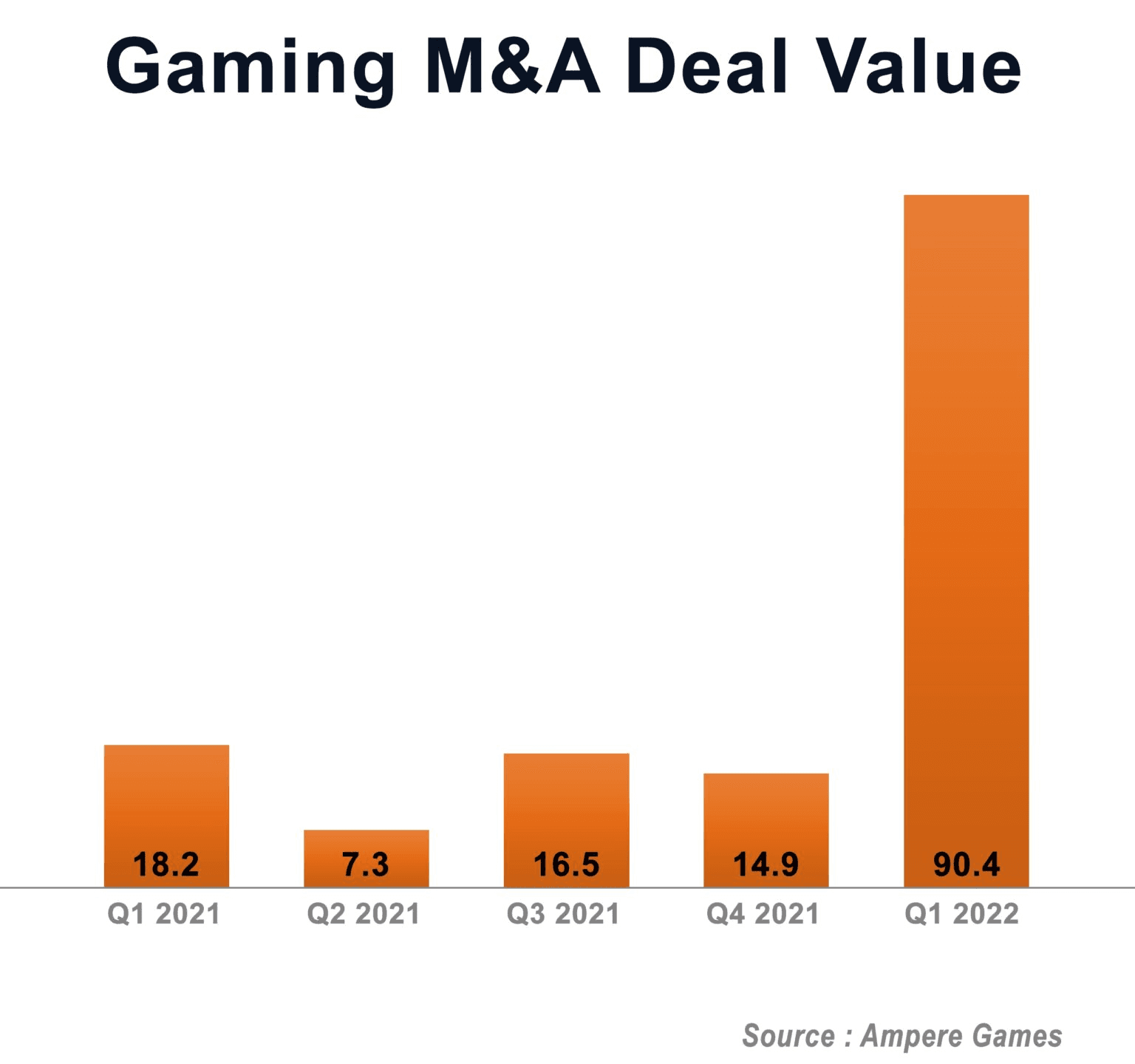

The industry is capitalising on this growth by consolidating: according to investment banking firm Drake Star, M&A activity reached a record $85 bn in 2021 – three times the value in the previous year – as game companies participated in 1,159 deals including 299 mergers and acquisitions. In the first quarter of 2021, the value of deals announced was $18.2 bn, and deal value mushroomed to $90.4 bn in the first quarter of 2022, on the back of Microsoft’s purchase of Activision Blizzard (the biggest ever acquisition in gaming), and Take Two’s deal with Zynga.

Global gaming revenue is projected to reach $321 billion by 2026, driven by mobile gaming and innovative offerings.

While industry observers agree that explosive growth is powering gaming consolidation today, they also argue that tech giants are fighting over the future of gaming through high-profile deals, and vying for supremacy in the industry. COVID transformed gaming forever, and the aggressive plays by tech powerhouses are the result of this tectonic shift. However, there is more to the consolidation today than just a bid for primacy or an investment in gaming’s future, as we will discuss below.

The COVID-19 pandemic caused a surge in gaming demand, but the subsequent return to normalcy led to a decline in revenue growth as the world adjusted, impacting industry performance and leading to strategic shifts.

Transformative Gaming Deals: Then and Now, Including Activision Blizzard

Throughout video game history, transformative deals have powered the growth of companies via the acquisition of lucrative intellectual property (IP). Ownership of valuable IPs has driven industry dominance and informed monetization strategies, expanding gaming franchises and related media products. The key difference between the deals of the past and the M&A today is the large sums of money involved, the strategic acquisition of acquired studios by large publishers, and the complex agendas behind consolidation. Large publishers such as Microsoft, Sony, and Tencent act as parent companies overseeing multiple studios, shaping market concentration and innovation. The surge in development budgets and development costs for AAA games has also played a major role, with budgets for franchises like Call of Duty and Grand Theft Auto exceeding $250 million and $300 million, respectively, and AAA game budgets now often surpassing $200 million. Some acquisitions before the pandemic period also reveal similar motivations, foreshadowing the billion-dollar deals that characterise gaming acquisitions today, such as Microsoft's $68.7 billion acquisition of Activision Blizzard—the largest gaming deal ever.

The IP-centric deals of the past

Many of the transformative gaming deals in the two decades prior to COVID center around the acquisition of lucrative IPs and the strategic expansion of company portfolios through acquired studios. In 1998, Take Two bought BMG Interactive, the then makers of Grand Theft Auto, for $14.2 mn. Take Two’s purchase eventually resulted in ‘the most lucrative game in history’ and the most profitable entertainment product of all time – GTA V. GTA’s ‘incredible staying power‘ has yielded billions of dollars in revenue.

In 2005 Bandai and Namco merged and became the third-largest gaming company in Japan after Nintendo and Sony, on the strength of their combined franchises. In 2011, Tencent became the majority shareholder of Riot Games, the makers of League of Legends, acquiring a 93% stake in the company for $400 million. Four years later it acquired the remaining 7%, owning League of Legends outright at a time when the game was rapidly becoming one of the world’s biggest esports. The game is hugely popular, especially in China, and League of Legends’s esports events are some of the biggest in the world.

In 2014, Microsoft acquired Mojang, the creator of Minecraft, for $2.5 bn – a prescient deal, considering that Minecraftwould go on to become the best selling game of all time, with 238 million copies sold across platforms as of 2021. Amazon’s acquisition of Twitch in the same year for $970 mn is an example of a pre-COVID platform play – Amazon not only had the capacity to sustain Twitch’s rapid growth, but it could also enter an entirely new platform – live streaming – and Twitch was eventually able to support a massive number of viewers and broadcast high-profile esports tournaments on the back of Amazon’s support platform. In 2021, the Dota 2 International finals drew in a total of 1.7 mn unique viewers on Twitch – 62% of the 2.7mn viewers who tuned into the game. Tencent’s 2016 acquisition of Supercell is not only one of the few high-stakes deals before COVID: it is also a platform play. The Chinese company made the third-largest gaming deal in history by paying $8.6 bn for a majority stake in Supercell, adding the Finnish developer’s flagship game Clash of Clans to its portfolio. The mobile title raked in nearly $490 mn in 2021 through in-app purchases. Tencent has consistently made the most of the mobile gaming platform – 60% of its $19.3 bn gaming revenue in 2019came from mobile games, and in Q2 2021, the company’s mobile games raked in $6.3 bn – 30% of all gaming revenue. Successful mobile game developers are often targeted for acquisition to enter fast-growing emerging markets like Latin America and India.

The Billion-Dollar Deals Today

Gaming M&A today are notable for the massive, billion-dollar amounts in play, and how they have catapulted companies into market-leading positions through the acquisition of both established and emerging acquired studios. In the past, Tencent’s buyout of Supercell or Activision Blizzard’s $5.9-bn purchase of King were the exception rather than the norm, but today, even the low-profile deals – such as EA’s acquisition of smaller mobile studios – run into billions of dollars. Mobile studios are now seen as strategic assets, allowing companies to diversify revenue streams and adapt to market challenges.

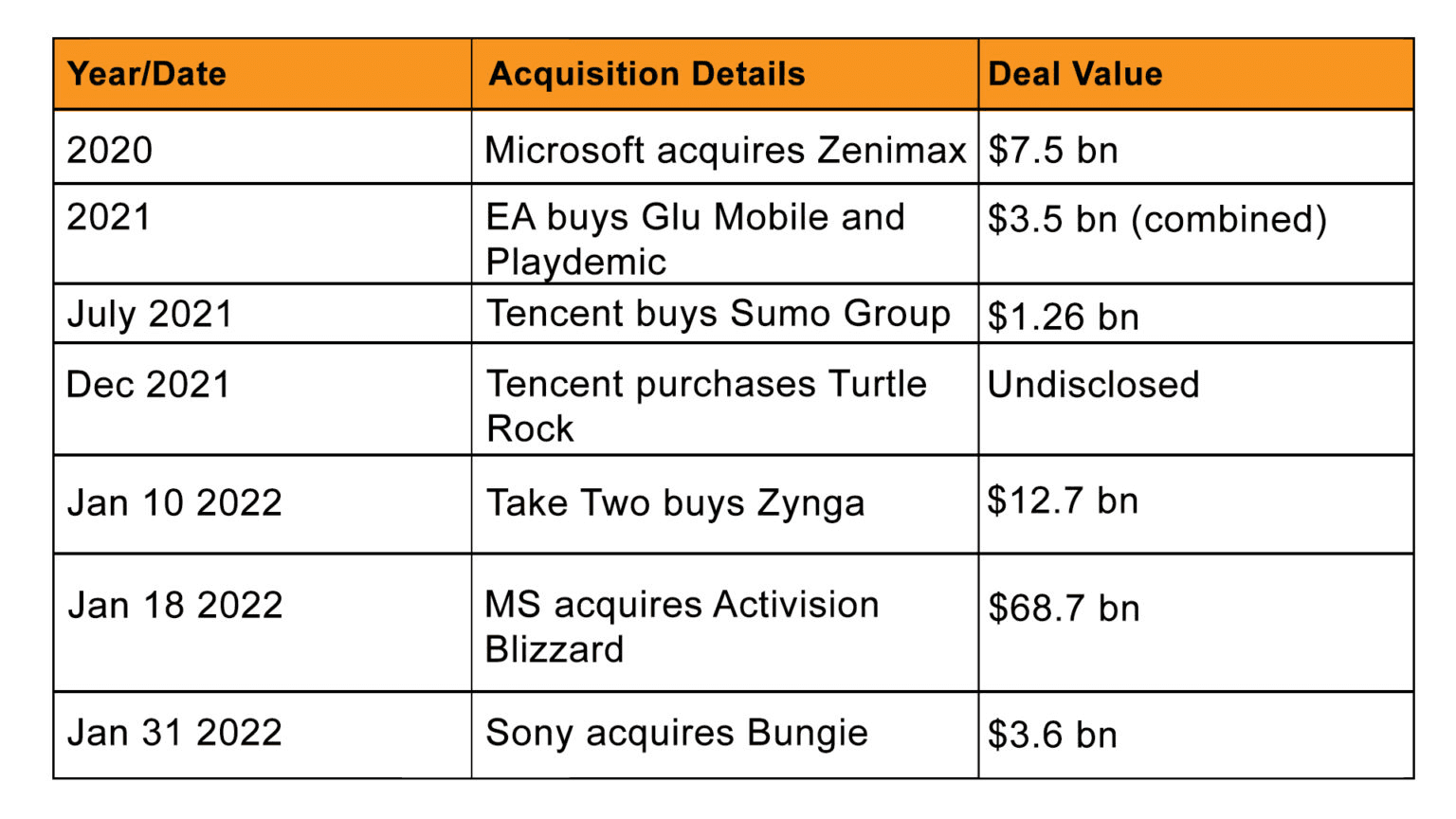

In 2020, Microsoft purchased Zenimax for $7.5 bn, giving it control over some of the world’s greatest franchises, such as Fallout, The Elder Scrolls, Doom and others.

Electronic Arts, the third-largest Western gaming company, has largely built its success on desktop and console titles. The studio bought into the mobile gaming market in 2021 with the acquisition of Glu Mobile for $2.4 bn in April 2021, followed soon after by the purchase of Playdemic for $1.4 bn. These acquisitions of mobile studios have expanded EA's portfolio and positioned it for growth in new markets.

But it was in January 2022 that the gaming industry went on a purchasing spree. Take Two acquired Zynga for $12.7 bn. Microsoft bought Activision Blizzard for a whopping $68.7 bn. When Sony acquired Bungie for $3.6 bn, its stock surged by nearly 6%.

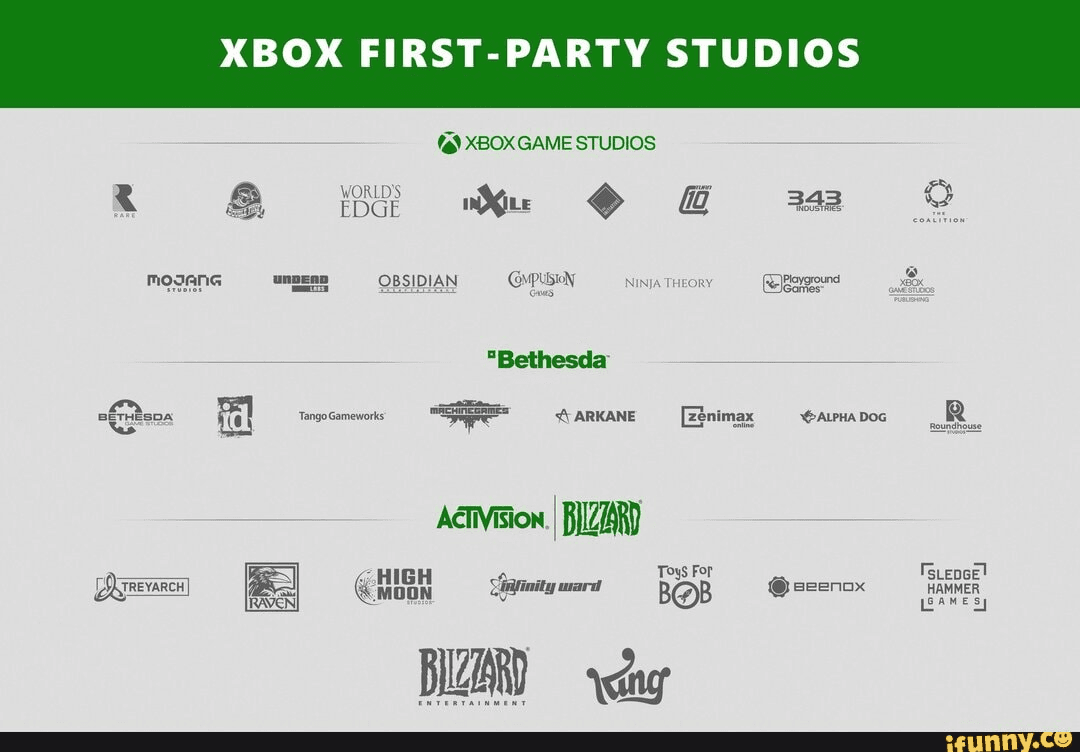

When Microsoft completed its purchase of Activision Blizzard, it announced that it was the third largest gaming companyin the world by revenue, behind Sony and Tencent. Microsoft now owns 24 first-party studios, while Sony owns 19.

Various reports have led to speculation that Ubisoft may be the next studio to be acquired. A Bloomberg article reports that a few private equity firms have been scrutinizing the business, and employees have also claimed that various company divisions are under audit. In 2018, the studio fought off a hostile takeover play by French company Vivendi, but Ubisoft’s CEO has said in a recent earnings call that the company is open to offers for purchase, amidst plummeting stock prices.

Rising development costs have significantly impacted development teams, leading to restructuring, layoffs, and changes in studio operations as companies seek to optimize resources and adapt to the evolving landscape of the gaming industry.

In the next section, we discuss the reasons why gaming companies are making such high-profile deals today.

Platforms, Metaverse, Tech and Users: Why the Industry is Consolidating

The industry’s M&A frenzy is not just about capitalizing on growth during the pandemic. By consolidating, companies are attempting to make their mark on new platforms, jump-start the metaverse, enrich gaming with new technologies and assimilate vast user bases spread out among multiple IPs and platforms. Many companies pursue mergers and acquisitions to gain access to new markets, technologies, or user bases, strengthening their competitive position. Major players are making strategic investments in mobile studios and AI tools to maintain competitiveness and mitigate risks. There is also a strategic shift underway, with companies adapting their business models through restructuring and project realignment in response to industry changes. Additionally, companies are investing in cloud gaming, metaverse, and Web3 platforms as part of the ongoing platform wars.

Platform Plays: Staking a Claim in Lucrative Platforms

The high-profile deals made by Take Two, Microsoft and Sony do share a common thread – the acquisition of first-rate IP’s. However, Take Two and Microsoft are also making multiple platform plays with their acquisitions, aiming to expand their reach across console, PC, and mobile—the three categories that define the gaming industry’s market segmentation.

Take Two grew on the back of console and PC gaming, powered by franchises such as Red Dead RedemptionGrand Theft Auto. It is now looking to grow on the mobile platform by acquiring Zynga, reflecting a strategy to compete across multiple platforms.

Take Two has unsuccessfully tried to build an in-house mobile gaming market strategy by acquiring small companies such as PlayDots. By buying Zynga, it not only owns money spinners like Farmville, but can also learn from Zynga’s expertise in making free-to-play mobile games. Take Two also plans to launch more of its franchises on mobile platforms – will we be seeing a mobile version of Read Dead Redemption in the coming years?

Microsoft’s acquisition of Activision Blizzard not only gives it ownership over World of Warcraft, but also mobile games such as Call of Duty Mobile. It also gains mobile games such as Candy Crush Saga, because Activision Blizzard acquired the social gaming company King in 2015.

Microsoft makes about $250 million per month from its 25 million Xbox Game Pass subscribers, and Game Pass subscriptions account for 80% of the tech giant’s gaming revenue. With Activision, Microsoft now has 24 first-party Xbox studios and can offer even more content on a subscription service already known as the ‘Netflix of gaming’, reaping ever-higher profits from its XBox division. Large technology and entertainment companies are increasingly seeking to secure exclusive content for subscription services like Xbox Game Pass or PlayStation Plus, intensifying the battle for user engagement.

And if that’s not enough, Microsoft boasts a steadilyimproving cloud gaming solution, Xbox Cloud Gaming. By purchasing Activision Blizzard and Zenimax, the tech giant could offer a wider variety of IPs on the cloud, drawing more users into its game streaming service and further strengthening its presence across multiple platforms.

The Chinese company Tencent has become the world’s largest gaming company by revenue largely on the back of its extensive portfolio of online games, targeted at its domestic audience. Games like PUBG Mobile and Honor of Kingsregularlyrank as top-grossing mobile titles, and as discussed above, its mobile segment has always been a rich source of revenue.

Now, it may be looking into desktop and console gaming. In 2021, Tencent acquired 11 gaming companies, including Turtle Rock (developers of Back 4 Blood) and Sumo Group (developers of many Sonic racing games). This is a bid to enter the console and desktop platforms, according to industry analyst Drake Star, which also expects the gaming giant to acquire many AAA studios and developers this year.

Platform plays are not restricted to high-profile deals – smaller acquisitions reflect similar objectives. Netflix is continually buying indie studios and adding to its gaming library in a bid to enter the mobile gaming sector, and it intends to use data from its gamers to enhance its video catalog as well. In a Gamopedia poll, 33% of the respondents expressed interest in playing games on the Netflix platform, while 26% said it depended on Netflix’s gaming library.

With increased competition in the gaming industry, including market saturation, higher user acquisition costs, and the proliferation of live service games, it is becoming more difficult for publishers to succeed and differentiate their productsacross these three categories.

The Metaverse: Jump-Starting the New Internet

The metaverse is a combination of virtual and augmented reality where users fully inhabit a simulated world created by technology, interacting with each other within digital environments. It is considered the future of the internet and cyberspace. It is still in its infancy, and it could take more than a decade for a full-fledged metaverse to come into being.

When Meta (formerly Facebook) acquired Oculus in 2014 – years before the company had sold a single headset – it was staking an early claim on the metaverse. As one of the 'big tech' players, Meta has also acquired many successful VR game studios, such as Ready At Dawn (the makers of the award-winning Lone Echo) and Beat Games (makers of the highly successful Beat Saber). These acquisitions are not just about adding IPs – but about offering more reasons to participate in the metaverse and ‘Social VR’. Meta’s Oculus has also acquired many companies to accelerate development of the metaverse by improving the VR experience. In 2015, it acquired Surreal Vision, which recreates 3D environments in virtual spaces. A year later it purchased Eye Tribe, which specialises in eye-tracking technology that allows you to control the direction you look using your eyes alone. Meta’s metaverse play has actually hurt profits and Reality Labs, the division behind augmented reality and virtual reality, lost more than $10 bn in 2021, despite impressive sales figures for the Oculus Quest 2 headset in the same year. This has not deterred investment in the metaverse.

Other big tech companies, such as Microsoft, are also expanding their influence in metaverse development and related Web3 marketplaces. According to Bloomberg, even Microsoft’s acquisition of Activision Blizzard is a metaverse play, because the company’s new IPs give it access to massive gaming communities, which have come closest to creating metaverse-like experiences. Both Roblox Corp, publisher of Roblox and Epic Games, the publishers of Fortnite, have organized immersive in-game experiences such as live concerts. Epic Games pioneered crossover events featuring an eclectic mix of IPs through custom skins. Such events were attended by millions, turning Fortnite into a metaverse community rather than just a battle-royale F2P game.

Media outlets have played a significant role in shaping public perception of metaverse investments and industry trends, often comparing current developments to past tech booms and scrutinizing the strategies of big tech companies in this space.

Technology First: Betting on the Cutting Edge

Sony’s reasons for acquiring Bungie, however, have little to do with the metaverse, but much to do with technical know-how: they want in on Bungie’s capabilities in live-game services, and its expertise with cross-platform play. The increasing complexity of game design, driven by advanced technology and higher player expectations, has significantly raised development costs for AAA titles. These rising development costs impact project viability and have led to budget surges, project cancellations, and changes in how studios operate. As a result, development teams are often restructured, with some studios reducing team sizes or consolidating resources to manage expenses. Sony has not delved into the live-service platform, opting instead for narrative-driven games and open-world franchises such as Horizon Zero Dawn. Buying Bungie gives Sony the chance to get into the live-service platform, and move past a console-only strategy – in fact, the company wants around half of its games on desktops and mobile devices by 2025, indicating a significant change in its approach to making and distributing games. The industry as a whole is transitioning towards mobile and live service games as a response to rising development costs and market saturation. Bungie has mastered the live service model after years of developing the Destiny series, which has drawn 187 million unique users over the course of its existence. Bungie also has pioneered cross-saves and cross-platform play, and has deployed a variety of revenue models to keep Destinycompetitive against other F2P and subscription titles. Bungie’s complex infrastructure supports almost a dozen different hardware platforms for Destiny 2, including Google Stadia. Sony could not have chosen a better tech partner. Bungie plans to extend Destiny beyond gaming as well – there is speculation that the company is working on a Destiny TV show or movie as part of its plans to create a Destiny Universe, just as Sony adapted The Last of US into a TV Show and Uncharted into a movie. Venturing into new mediums will draw more users toward Sony and Bungie’s franchises, and Sony may well lean on Bungie’s expertise in coping with enormous player communities. Square Enix has sold off its western titles to focus on technologies such as the blockchain, AI and the cloud. Square Enix’s deal with Embracer Groupinvolves the sale of 50 IPs, including classics like Tomb Raider, Deus Ex, Thief and Legacy of Kain, for just $300 mn. However, the company still has a strong library and has also retained some of its Western IPs. Its decision to focus on new tech could enhance their gaming titles as well.Prior to the sale of its IPs, Square Enix invested in the Ethereum-based game developer TSB Gaming, creator of The Sandbox, a virtual world built on the blockchain, which allows players to build, own and monetize their voxel gaming experiences. Square Enix’s president Yosuke Matsuda has emphasized the company’s interest in introducing blockchain technologies into gaming to incentivise gamers and modders, and the gaming firm may also look into including token economies in its titles. The sale of Western IPs will bankroll these endeavours.

Gaining User Communities and Data

Consolidation buys access to millions of users spread out among the popular franchises of smaller studios, and these user bases yield significant data-driven insights. This enables bigger players to devise well-directed promotion strategies across an ever-increasing portfolio of games and first-party studios, thereby saving costs on marketing and ad campaigns. User acquisition and retention is a high priority across gaming platforms and a significant part of a game app's marketing strategy. Microsoft not only gains lucrative IPs by buying Zenimax and Activision Blizzard, but it also buys into vast user bases and data across platforms such as desktops, consoles and mobile.User acquisition is vital to the metaverse – big players are already taking notice of the huge user communities of Roblox and Fortnite and their metaverse-like experiences. Having access to data on these communities, their behaviour and their metaverse expectations might be a game-changer for tech giants who are looking to usher in the new internet. Gaining users and their data will hence allow gaming giants to fine-tune their consolidation agendas. Indeed, user data and insights into behaviour tie into all the three objectives listed above: they will enable companies to maximize gains from new platforms, entice gamers into a new, as yet unpolished metaverse, and improve the user experience with new technology.

Impact of Consolidation on Gaming

Today’s gaming deals are not solely about acquiring high-performing IPs – companies have a complex agenda, ranging from platform plays to metaverse investments. In this section, we discuss how gaming could change as a result of such strategic moves

More monopolies and exclusives: Microsoft’s acquisition of Activision Blizzard was not met with unanimous approval, and raised concerns that the tech company had suddenly risen to a position where it could dictate terms as a monopoly player with the largest number of first-party studios. Microsoft’s position of power over the gaming industry may also draw antitrust scrutiny according to some observers. Such larger players can also decide to keep lucrative IPs as exclusives – note that XBox chief Phil Spencer has all but confirmed that The Elder Scrolls VI will be an exclusive available only on XBox and PC.

Rising interest rates have made funding more expensive and less accessible for video game companies, slowing down big-budget AAA projects and further accelerating industry consolidation. At the same time, shifts in consumer spending—driven by economic pressures and changing post-pandemic habits—have reduced discretionary spending on games, intensifying challenges for both established and emerging studios.

The consolidation trend is leading to a more concentrated and capital-intensive gaming industry, dominated by a few major players. This has resulted in significant layoffs, with an estimated 45,000 jobs lost from 2022 to July 2025, disproportionately affecting junior staff and raising concerns about the future talent pool and diversity in the sector. The wave of layoffs has also led to the cancellation of several video games and the closure of numerous studios.

Tech giants vs smaller players: Big companies have made gaming acquisitions that will cement their place as market leaders. This will make it harder for smaller studios to compete, but not to create, as they will get opportunities to be purchased in an industry that hungers for new talent and new experiences. Netflix has bought many mobile game studios, and Meta has done the same for VR game studios. However, industry behemoths may not allow such creators to maintain their independence. Studios with successful franchises may succumb to acquisition after a few failed experiments hurt their bottomline, and the dominance of a few large players may stifle innovation and the creative freedom of developers working within the confines of a larger corporate structure. In effect, smaller studios can still create in an era of consolidation – but what they create may be dictated by their corporate paymasters rather than their creative ambition, leading to less variety in gaming content.

Market saturation is also a growing concern, with platforms like Steam now hosting over 80,000 games, making it increasingly difficult for new titles to stand out. As video game companies continue to acquire studios, such as the recent acquisition of Gearbox Entertainment—known for valuable IPs like Borderlands—portfolio diversification becomes a key strategy for maintaining market control and expanding reach.

Rising economic costs for consumers are another consequence of industry consolidation. By late 2025, base game prices are expected to reach $80, and subscription costs for gaming services are also projected to increase, placing additional financial pressure on gamers.

Cross-platform play as the norm: The gaming industry has traditionally not been very keen on providing cross-platform playability. However, this is likely to change because of the various platform plays reflected in today’s gaming M&A. Thanks to its acquisitions, Microsoft already boasts a sizeable collection of games playable via the Xbox Game Pass and its cloud platform. Sony is looking to enter the live-service online platform with the help of Bungie. Take Two wants to launch mobile versions of its famous IPs. As the number of multi-platform franchises grows, cross-platform play could become the norm rather than the exception. At the very least, gamers can expect an enhanced cross-platform experience going forward.

Mobile gaming as default: Smartphones are already the most popular device for gaming, but the introduction of high-quality IPs on mobile platforms could make smartphones the default device for gamers, or at least provide an experience that transcends casual gaming. As cloud gaming on mobile matures, more subscription-based services featuring high-quality games can be accessed purely via smartphones – without any hardware apart from the mobile screen. In the future, a smartphone streaming to a HD screen or a headset may be all that you require to get a high-fidelity, immersive playing experience. Gaming could hence become ‘mobile-native’.

Forging the Metaverse and its community: Apart from its technological trappings, the metaverse is essentially an online interconnected space where individuals interact with each other. Acquiring gaming companies that have experience dealing with massive user communities, rather than just user bases (contrast WoW players vs Windows users), will enable tech giants to understand how to create the metaverse community. In many respects, WoW can be considered a successful proto-metaverse – from its earliest stages, it featured player-driven economies, social gathering points and virtual real estate. Technology companies are looking to integrate the immersive elements of gaming into the metaverse experience: Roblox, Epic Games’ Fortnite, and GTA Onlinealready have metaverse-like platforms that incorporate player communities into their business models.

Conclusion: How Consolidation will Beget Consolidation

Microsoft's purchase of Zenimax in 2020 sparked speculation that there would be more such major acquisitions in the future – and this has proved to be true.

Tech companies and game industry giants have harnessed COVID-period growth to make billion-dollar consolidation deals. To some observers, the consolidations are still very much underway and experts suggest that we are entering an era of mega-consolidation, where consumer demand for cross-platform experiences will drive further M&A. Even tech firms without a presence in gaming may enter the market because of the industry's massive potential – 26% of the world's population plays games and gaming is the most lucrative entertainment industry by a wide margin.

Acquisitions lead to acquisitions, according to analyst Brandon Ross. Successful publishers and studios can expect to be bought – the industry may become the fief of a few large players, but studios that create quality games will not lack for customers, be they gamers or tech giants.

Mergers and acquisitions are about spending money to make money. Big players can create or simply buy more content. With more content comes more players, and with more players arises the need for more and diverse content – a virtuous cycle where high-profile acquisitions constantly transform the gaming market so that it can keep pace with rising consumer expectations and the demand for more content.

The consolidation in the gaming industry may eventually propel it toward a new normal, with a thriving metaverse and a tech-enriched gaming experience that transcends platform limitations. For gamers, developers, independent studios and gaming giants, that is a win-win situation.

With over 30 years in gaming, from NES classics like Mario and Contra to modern platforms like PS5; I specialize in analyzing game mechanics and building game taxonomy. I also enjoy brainstorming innovative game concepts, continually exploring the vast possibilities within game design.